Whatever the effects of political incentives and rent-seeking in MEGA’s economic development efforts, MEGA decisions no doubt usually involve good faith efforts and research by MEGA officials and the business recipients of the MEGA grants. Nevertheless, even this is not likely to advance MEGA’s goal of accelerating job growth above what would have been generated by the market alone. We say this because MEGA officials face an inherent "knowledge problem" that is widely recognized in the economic literature: They cannot reliably determine which corporations will bring the most benefit to the state.

True, most people think of this as a problem that can be solved with good financial research and foresight. But in the book "The Fatal Conceit: The Errors of Socialism," Nobel Memorial Prize-winner F. A. von Hayek explains that "the curious task of economics is to demonstrate to men how much they really know about what they imagine they can design."[163]

He then illustrates the limits on the transmission of information and knowledge that can be accumulated by any small group of planners. Hayek recognized that knowledge is highly diffused and contained in the minds of millions of economic actors who are working to maximize their own self-interest.

The market is the only known method of providing information enabling individuals to judge comparative advantages of different uses of resources of which they have immediate knowledge and through whose use, whether they so intend or not, they serve the needs of distant unknown individuals. This dispersed knowledge is essentially (Hayek’s emphasis) dispersed, and cannot possibly be gathered together and conveyed to an authority charged with a task of deliberately creating order.[164]

In other words, regardless of how talented they are, it is impossible for state officials to know how to redistribute resources in such a way that would make society better off than if they had not intervened. At best, they can hope to get lucky.

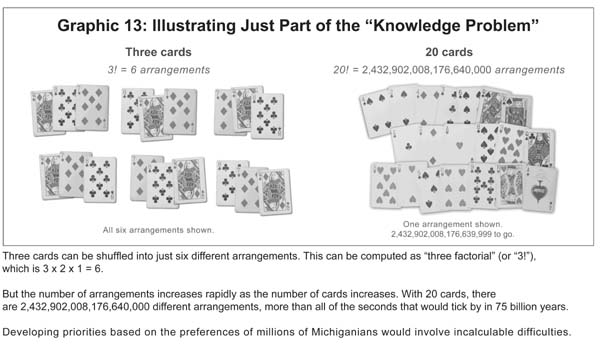

To see just how lucky they would need to be, consider the following illustration, devised by the respected Stanford University economist Paul Romer, which helps explain the difficulty in commanding and using information.

There are only six ways to arrange three items (see Graphic 13 above). You can calculate this by using a simple "factorial," where "three factorial" (or "3!"), simply means 3 x 2 x 1, or 6.

But increasing the number of the cards increases the number of potential arrangements at a dramatic rate. With just 20 items, the number of arrangements rockets to 2,432,902,008,176,640,000 — over 2 quintillion, and more than all of the seconds that would tick by in 75 billion years (2,365,200,000,000,000,000).

Now extend that concept to a full deck of 52 playing cards. It is conceivable that some theoretically possible arrangements of a card deck have never actually occurred in any card deck in all of human history.

Yet when economic development officials survey the state economy and try to add more jobs to the state employment rolls than would otherwise exist, they are dealing with potentially millions of items to prioritize, including the varied preferences and plans of the state’s business firms and consumers. Moreover, as Hayek noted, this knowledge is essentially dispersed in people’s minds; it cannot be gathered in the first place.

Track Record of the Private Sector

Thus, even the highest paid and most experienced Wall Street investment experts with scores of analysts at their disposal have trouble picking winners and losers in the marketplace. Ben Warwick, in his book "Searching for Alpha: The Quest for Exceptional Investment Performance," observes that between 1995 and 2000, "Of the 45 largest stock funds, only one has beaten the Standard and Poor’s 500 index . . . and that fund outperformed by a scant 0.60 percent per year."[165]

This is not an uncommon finding. Despite every conceivable advantage in divining which companies are good investments and which are not, and despite enormous economic incentives to succeed, even professional money managers rarely outperform the marketplace as a whole.

In 2002, then-MEDC CEO Doug Rothwell told the managing editor of The Observer Newspapers, "Our philosophy is to support winners, the companies that have a good business model."[166] It certainly sounds like a good strategy, but it’s the strategy employed by most professional investors, and they don’t usually beat the marketplace.

MEGA faces the same "knowledge problem" that plagues central planners in other governments and that makes it hard for private investors to outperform the Standard & Poors Index. They cannot somehow survey the marketplace and a sea of human interaction in all its detail, and then improve it through some state effort, such as targeting tax relief to corporations. It requires knowledge that can never be gathered, assembled and organized. Only millions of individuals acting freely can coordinate the many pieces of local knowledge into a system that is reasonably efficient at improving human wealth.